Lenders stress portfolio management as originations rise

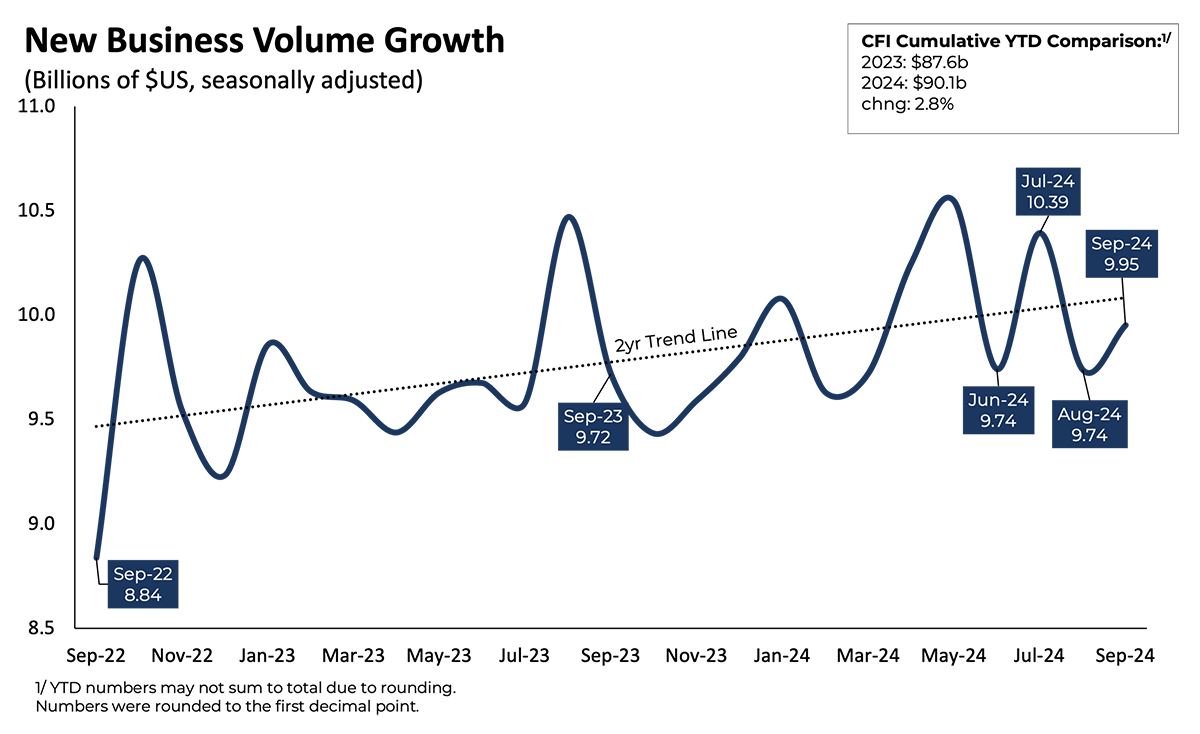

New business volume neared $10B in September

The equipment financing climate is heating up, but lenders are cautious, facing potential challenges tied to portfolio quality and compliance.

New business volume in the equipment finance industry increased 2.2% in September to nearly $10 billion, according to the Equipment Leasing and Finance Association’s (ELFA) CapEx Finance Index, released Oct. 24.

Some lenders are capitalizing on technology such as AI-driven automation platforms to expedite transactions and accommodate new borrowers, Neal Garnett, chief commercial officer at global equipment financier DLL, told Equipment Finance News.

“There is more speed than ever before, and I think that has an immediate impact on a finance company,” he said during the recent ELFA convention in Austin, Texas. “We have a large-flow business with hundreds of thousands of transactions, and customers want an Amazon Prime-type experience.”

DLL’s new business volume is up 15% to 20% this year, indicating that the industry is in a better position than a year ago, when high interest rates and inflation kept many prospective borrowers on the sidelines, Garnett said.

Meanwhile, credit approvals fell 70 basis points in September to 75.6%, according to the ELFA report. The total headcount for equipment finance companies rose 1%.

Banks big on credit performance

Easing inflation and expectations of continued interest rate cuts by the Federal Reserve have contributed to increased lender confidence in recent months. While independent lenders work to beef up their portfolios, larger institutions are prioritizing portfolio management, Daniel Devries, managing director at Wells Fargo Equipment Finance capital markets team, told EFN during the conference.

“Credit performance is really holding steady, with very strong portfolio metrics sort of being reported across the bank sector,” he said.

With equipment purchasing expected to ramp up next year, other lenders should also make sure their portfolios are “stabilized and delinquencies are not continuing to rise” before aggressively pursuing new customers, Wintrust Specialty Finance President and Chief Executive David Normandin said at the conference.

“We make money by people paying us back, so I’m always thinking ahead,” he said. “So, what do I think the risk is for the next couple years? I think it’s around portfolio quality and what that continues to look like.”

Regulatory roadblocks ahead

Regulations are challenging the equipment finance industry, including Section 1071 of the Dodd-Frank Act, which requires financial institutions to collect and report data from applications by small businesses to the Consumer Financial Protection Bureau, DLL’s Neal said.

“Compliance and regulations are becoming more of a thing in our industry,” he said. “Knowing your customer sanctions list, Ultimate Beneficial Owner rules, Dodd-Frank 1071 requirements, all of that stuff creates potential friction and slowness in something that customers want to be fast.”

Adhering to regulations while keeping transactions seamless will be key for lenders moving forward, Neal said.

Basel III, international rules that require banks to have enough capital and liquidity to absorb unexpected losses, is another potential hurdle for equipment financiers, Wells Fargo’s Devries said. These measures aim to strengthen the regulation, supervision and risk management of banks.

“Banks will need to be nimble to take care of their clients while still staying compliant with the Basel III rules,” he said.

Basel III is slated to take effect in July 2025 and will apply to banks with at least $100 billion in assets, according to accounting and consulting firm Forvis Mazars.