Demand for construction equipment weakens

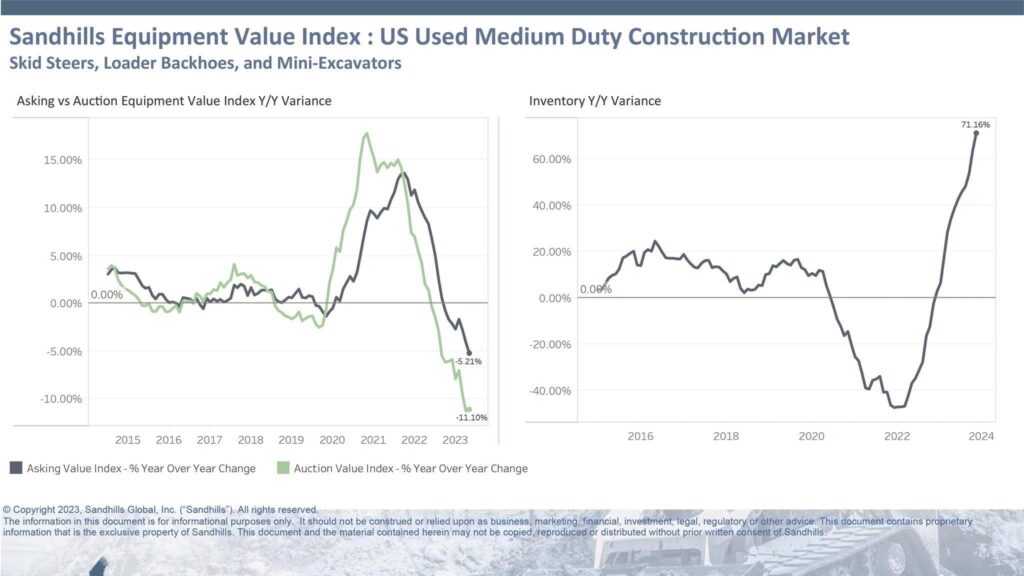

Medium-duty construction equipment retail values down 5%

Demand for construction equipment softened in November as auctions, dealers and OEMs continued to manage excess inventory.

Growing inventories amid slowed demand continued to push down construction values in November, Jim Ryan, equipment lease and finance manager at Sandhills Global, told Equipment Finance News.

“The demand is lower than normal on the used side, which is different for construction,” he said. “You’re seeing some of the numbers come down and soften on the asking and the auction side.”

Part of the reason is some buyers are waiting to see where the market and macroeconomic conditions go next year, Ryan said.

“There [are] a lot of people sitting on their hands not doing a whole lot,” he said. “With inventory levels being up there, no one wants to go next year with overloaded inventory.”

John Deere projects sales to be down by around 10% next year, while the company expects shipments to decline due to inventory build, Director of Investor Relations Brent Norwood said during the company’s Nov. 22 earnings call.

“We did build some inventory, but certainly not at the pace that the broader industry did,” he said.

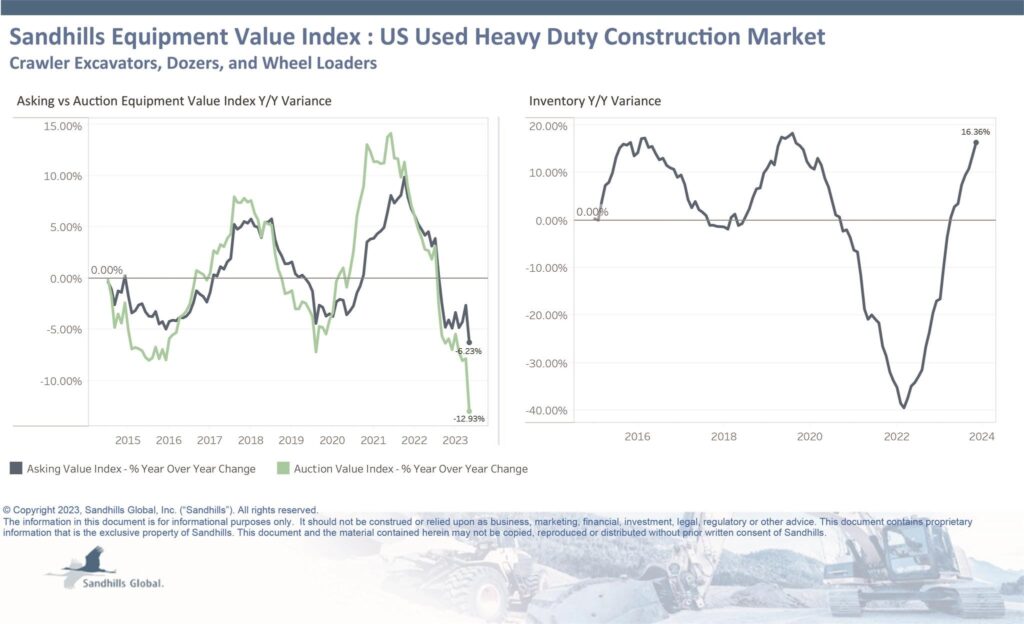

Heavy-duty construction values fall

Sandhills Global market values for used heavy-duty construction equipment fell in November, as increased inventory for excavators, as well as dozers and wheel loaders, drove down values:

- Retail, or asking, values dropped 3% month over month and 6.2% year over year;

- Auction values declined 4.6% MoM and 12.9% YoY;

- Inventory increased 2.1% MoM and 16.4% YoY.

“Excavator inventory, as far as the heavy-duty side, has probably been the biggest driver in numbers as you see inventory climbing up in that space,” Sandhills’ Ryan said.

Medium-duty values more stable

While Sandhills’ used medium-duty construction demand also declined, values were more stable than heavy-duty construction:

- Retail values declined 1.4% MoM and 5.2% YoY;

- Auction values inched down 0.1% MoM and 11.1% YoY;

- Inventory rose 5.5% MoM and 71.2% YoY.

“On the medium-duty side, we’re starting to see things recover post-pandemic as far as inventory levels go,” he said. “It‘s a different dynamic with that side, but you’re not seeing a lot of demand be there.”

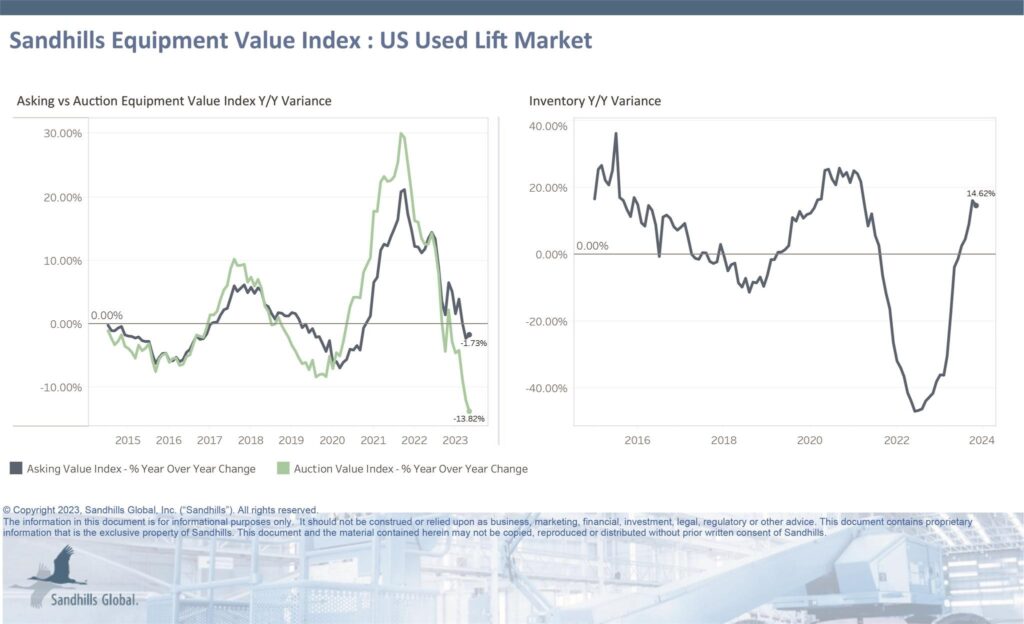

Lift values dip

Sandhills’ lift data remained mixed in November as the more niche construction market has yet to feel the same impact as the wider construction industry:

- Retail values for used lifts rose 1.4% MoM but remained down 1.7% YoY;

- Auction values dipped 1.4% MoM and 13.8% YoY;

- Inventory jumped up 3.2% MoM and 14.6% YoY.

“Inventory levels are starting to tick up on the lift side, but not as volatile as the rest of the construction world,” Ryan said. “Lifts are more of a specialty niche market within the construction industry. You’re continuing to see the supply chain ramp up.”