CHARLOTTE — Slower growth is likely in the U.S loan market this year, but businesses remain steadfast despite concerns of a recession.

“I’m getting more and more feedback from business contacts that 2023 looks like a growth year, but a muddling-through type of growth here,” said Martin Lavelle, senior business economist at the Federal Reserve Bank of Chicago, at Equipment Finance Connect in Charlotte on Tuesday. “Not a lot of ‘oh my gosh, the sky is falling’ kind of thing, but just planning to get through this year and then we’ll see where we’re at in 2024.”

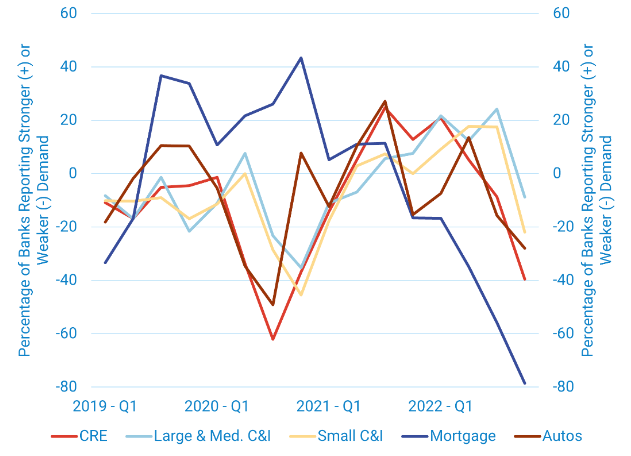

Lavelle also pointed to the Fed’s Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) as an indicator of potential economic activity.

“That’s not to say that economic activity is slowing or even decreasing in some sectors, and that’s what the Fed’s Senior Loan Officer Survey speaks to,” Lavelle said. “This is a survey of financial institutions that asks a number of things, but one of them is whether or not demand is strengthening or weakening for different sectors for loans going forward.”

“We see now, especially with the most recent data in the fourth quarter of 2022, more financial institutions are reporting weaker demand for these different instruments than stronger demand. Mortgage lending has led the way and given the rise in mortgage rates, commercial real estate is next as far as weakness, and [commercial and industrial] has really just turned negative.”

While rising rates are causing demand for loans to decline, customers are not tapping into lines of credit, Lavelle said.

“Talking with contacts, activity is slowing, demand has slowed, but then it’s also that problem customers or problem clients aren’t growing … nobody’s tapping into their lines of credit,” Lavelle said. “They’re slowing, but it’s not in the way of financial distress for these borrowers, so again: slower growth, maybe a little weakness, but not distress.”